Above and Beyond Tax-Advantaged Retirement Options

You’re meeting with an affluent client or prospect that is 10 years or less away from retirement. He’s in good shape financially, but he’s also in great shape physically, and wants to maintain his lifestyle for a lengthy retirement. However, he’s already maxed out his tax-advantaged retirement options and doesn’t want any more exposure to the stock market. The tax advantages of life insurance and the upside potential of indexed universal life insurance (IUL) can help him save extra income for retirement.

Here’s an outlay of how you can sculpt a strategy to address your client’s concerns and help them take advantage of the intrinsic tax advantages associated with life insurance.

In this situation, the client is a 50- to 60-year-old man who has maximized his other retirement income options, but still has some extra funds he wants to put toward retirement. He has an extra $100,000 of annual discretionary income ($8,333 per month) available each year for the next seven years, and wants to purchase or put his money in a vehicle that will make it sing during his retirement years. What should he do?

“Contributing to alternative, non-capped vehicles that can grow in a tax-deferred manner is often far from obvious to clients.”

Client Considerations

Retirement Plan Taxation Your client has assets in tax-deferred retirement plans in which withdrawals will be taxed, and in various securities where gains incur taxes. Often, clients are unaware they can contribute to alternative non-capped vehicles that can grow in a tax-deferred manner because it’s made far from obvious to them. Life insurance not only provides tax-free growth on gains, but also on distributions.

Accelerating Tax Obligations If the client is at least age 59 ½, he or she can begin withdrawing funds from a tax-advantaged retirement account or annuity, pay the taxes on those distributions, then allocate the funds to a life insurance policy. Those same funds can accumulate tax-free, while withdrawals from the policy’s cash value will also not incur income taxes. Essentially, this strategy allows the client to reduce future tax obligations when they get older, which may help if future health concerns arise.

Estate Taxes The client’s current estate may incur estate taxes if he or she passes away in the next few years. The client and his or her heirs may benefit from a life insurance policy death benefit to cover some of the estate tax expenses.

Legacy Giving Often, clients wonder what approach is the most responsible way to give back? By utilizing life insurance as a tool to help a philanthropic endeavor flourish, a client’s investment can exponentially grow and fulfill charitable commitments.

Approach Your Clients

Those who can benefit from this strategy most commonly fit the description of households with dual incomes, as they can more easily swing the yearly expenditure. However, families whose children have recently graduated from college, have paid off their mortgages or receive lump sums of inheritance from family, may also have the required surplus discretionary income necessary for this strategy.

Introduce your client to the potential of indexed universal life insurance (IUL) as a way to supplement retirement income. In this strategy, the client is the owner and insured of the policy and can name a spouse, family member, trust or philanthropic foundation as the policy beneficiary(s). The policy’s flexibility allows the client to fund it for seven years, and then draw an annual income. Because of the upside potential with no downside market risk of an IUL, the policy’s cash value has the potential to provide several years of retirement income and a death benefit for loved ones.

Course of Action

1. The client purchases an IUL policy with their discretionary income. The upside potential and no direct downside market risk of an IUL provides the potential to accumulate enough cash value to supplement the client’s retirement income. Make sure the policy has an over loan protection feature or rider to help protect the client from lapsing the policy when withdrawals are taken.

2. The client will max fund the policy, paying an annual premium amount just below the IRS Guideline Premium Limit to avoid the policy becoming a Modified Endowment Contract (MEC), which could adversely impact the policy’s tax advantages. The client pays this premium amount for seven years.

3. After year seven, the client should reduce the policy’s face amount. This allows the client to withdraw a higher amount of income because a lower face amount requires less cash value to support the policy and keep it in-force.

4. After year seven, the client can begin withdrawing tax-free, supplemental retirement income to use as they wish.

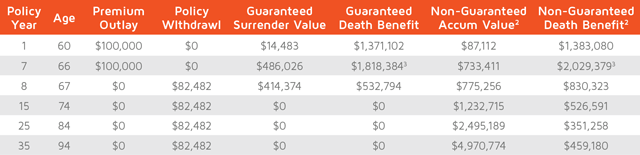

Hypothetical Case Design1

Client: 60-year-old male, preferred non-tobacco Initial death benefit: $1.296 million Initial premium outlay: $100,000 annually for seven years ($700,000 total) Non-guaranteed accumulated value at the end of year 7: $733,000 (based on a 7% illustrated rate) Guaranteed accumulated value at the end of year 7: $486,000 Annual distribution in policy years 8+: $82,482

Call your CreativeOne Life Sales Team at 800.992.2642 to develop a strategy and approach a prospect today. We’ll help coach you on a conversation starter and assist in providing the tools you need to win over a new client.

FOR FINANCIAL PROFESSIONAL USE ONLY. NOT FOR USE WITH THE GENERAL PUBLIC.

LF-0133 2015/5/5

1 The policy used for this hypothetical example is Eclipse Indexed Life (06-700 or ICC09-700), a flexible premium universal life insurance policy issued by Minnesota Life Insurance Company.

2 Non-guaranteed values are based on a 7% annual illustrated rate. In addition, money allocated to the indexed accounts is illustrated in a manner to receive an additional non-guaranteed 10-year rolling index credit bonus. The illustration shows the impact of a 1.00% bonus for policy years 11 + on all index credits received in the previous 10 years ending at the prior policy anniversary.

3 After Year 7, the policy’s death benefit option change based on withdrawals

Withdrawals will reduce the guaranteed death benefit. Surrender charges may apply to withdrawals. Taxation normally required, based on any gain at the time of surrender or transfer.

This is a supplemental illustration, values and rates may not be guaranteed and actual results may be greater or less than those shown.

Related terms: Case Consulting, Case Studies, Estate Planning, Financial Planning, Life, Qualified Plans, Sales Strategies, Uncategorized