How does diabetes affect underwriting? Diabetes Mellitus describes a group of metabolic diseases where the blood glucose (blood sugar) is elevated due to inadequate insulin production and/or body cells that do not respond properly to insulin. Individuals with diabetes often experience frequent urination (polyuria), increase thirst (polydipsia), and frequent hunger (polyphagia). There are two main… Read More

CarlCathey-ChiefUnderwriter,ConciergeUnderwriting Creative Edge

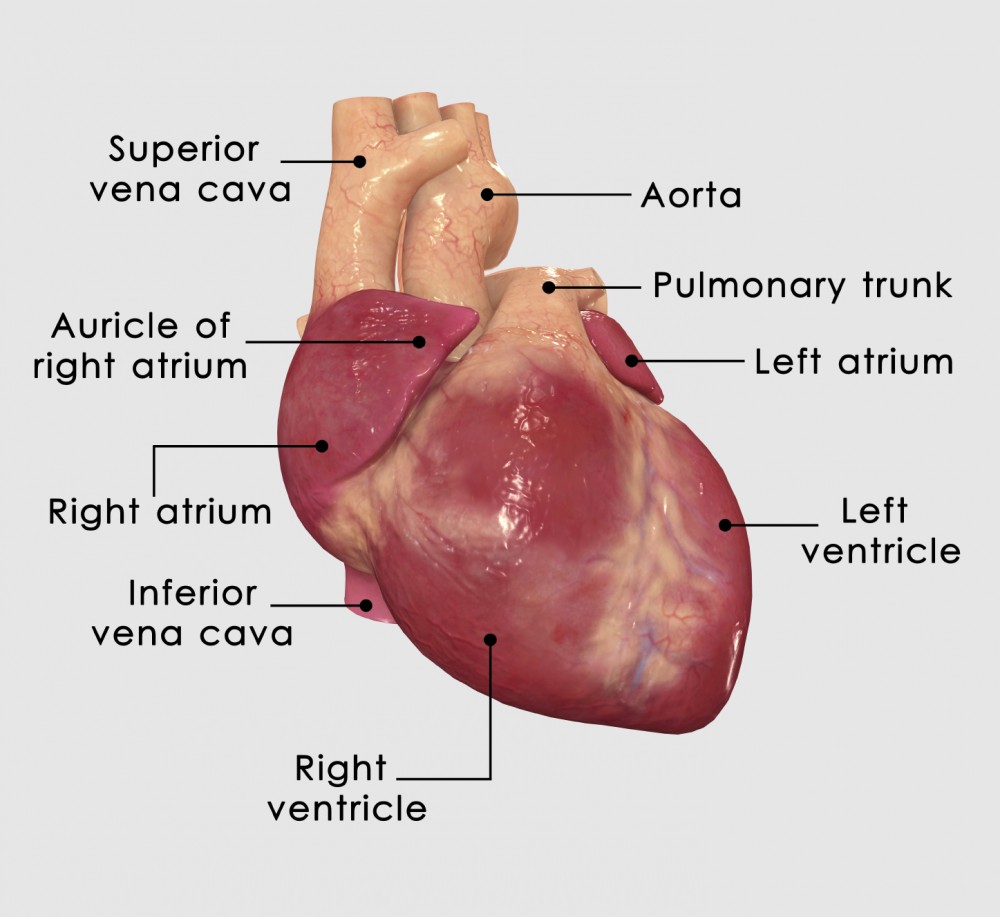

“I Gotta Guy” with Atrial Fibrillation (AFib)

Increasing cases of Atrial Fibrillation, also known as AFib, are being diagnosed every year. Therefore, you will likely see more clients with a history of AFib. We as field underwriters should be prepared to recognize AFib, symptoms, and types of treatment. AFib is an irregular and often rapid heart rate that commonly causes poor blood… Read More

“I Gotta Guy” With Prostate Cancer

#2 Cause of Death in Men, But Not a Foregone Life Insurance Conclusion Many men think purchasing life insurance is not possible following prostate cancer detection and treatment, but for some the option to purchase life insurance is a not a foregone conclusion. As you encounter potential clients with a history of elevated PSA or… Read More

Field underwriting tips for clients with peripheral neuropathy

Symptoms, causes, complications, treatments, prognosis, prevention. In the medical world, there are many things to consider when treating a patient. As an insurance agent trying to get a policy placed on a client with a medical condition, your job is much the same – to make sense of it all and present the underwriter with… Read More

“I Gotta Guy” Who’s Not Financially Justified?

If not handled properly, financial matters can create sticky situations both in our personal lives and our professional ones. Whether determining how to pay the bills or how a business is going to protect its interests, individuals and families have lots of important financial decisions to consider. If you have business owner clients, one of these financial decisions may be to purchase key person insurance on an employee who’s crucial to the success of the organization. Yet proving the need and being able to financially justify the amount of coverage desired is an important component of the underwriting process for any business case. As the agent, it’s critical for you to have the knowledge and know-how to step in and get the policy placed.

“I Gotta Guy” With Family History

Nature or nurture? The age-old debate has raged on for decades regarding just how we’re impacted by our genetics and our environment. As scientists continue making breakthroughs in DNA testing, we’re starting to better understand how our genetic makeup – and therefore our family ties – affects our health. Some 20 years ago in the insurance business, family history had little to do with underwriting outcomes. Today, this critical component of an individual’s overall picture of health is one that needs to be investigated and well-documented to ensure favorable offers are generated for every client.

“I Gotta Guy” With A Rated Case

As a life agent, you’ve experienced the joys of having cases come back as applied for and delivering the good news to clients. On the other hand, you’ve probably felt the frustration and disappointment that can come with helping a client apply for a policy only for the case to come back rated. These rated cases, formerly known as substandard cases, result in you having to talk with your clients about paying higher premiums or you having to do more work (obtain more information on the client’s health, shop the case or move on altogether if the client declines the offer) to get a policy placed.

“I Gotta Guy” With Ulcerative Colitis

In working with clients who have chronic conditions, it’s important that you understand and manage their expectations – just as they have to understand and manage their symptoms. Certain types of these conditions are highly treatable and can result in strong offers from carriers, but it’s critical that you perform due diligence in learning about the client’s individual situation and outlook. Ulcerative colitis, commonly referred to as UC, is an example of one we are starting to see more frequently on applications from our agents. Ulcerative colitis is a type of inflammatory bowel disease (IBD) that can cause long-lasting inflammation of the digestive tract and ultimately affect the lining of the large intestine, or colon. UC can closely resemble Crohn’s disease in terms of symptoms but can require very different treatment. Both can be debilitating and even life threatening depending on the severity of one’s symptoms, the progression of the condition over time and its potential complications. Clients with UC often experience severe or repeated pain in the abdomen without any explanation, a change in bowel movement and excretion, and weight loss.

“I Gotta Guy” With Lymphoma

Recently, we’ve seen a large number of lymphoma questionnaires from agents needing guidance on quoting these cases. As a result of this unusual volume, we’d like to present the following information to assist you in field underwriting clients with these challenges.