College for one, retirement for the other

Do you have grandparents looking for ways to financially help their grown children or grandchildren? Next time you meet with those clients, offer a way they can help provide an income stream for their child’s retirement and an incentive for a grandchild to finish college using a cash accumulation strategy with an indexed universal life insurance (IUL) policy.

Client Profile

Grandparent(s), approximately age 55 to 75 who are required to take RMDs, want to reduce estate liability or have funds they wish to pass to another generation. They can take advantage of current gifting limits ($14,000 per person; $28,000 per couple). The ideal candidate has a son or daughter in his or her mid to late 30s with a child between the ages of 0-5. The grown child could:

- Be divorced or widowed

- Be a single parent

- Have a standard of living significantly lower than the parents

- Have difficulty making retirement contributions because of reduced salary, child support, alimony, unemployment or a large amount of debt

Potential Client Concerns

- Need for a college graduation incentive – The grandparents want to provide an incentive to a grandchild to graduate from college. They like the idea of providing a cash “bonus” as a graduation present, which their grandchild can use for paying down student loans, a home downpayment, vehicle purchase, or other expenses.

- Ease the burden of college saving – With the escalating costs of college, the grandparents want to help provide supplemental funding for their grandchildren.

- Providing for the grandchild in the event of their child’s death – The grandparents want to help their grandchild save for college and provide for his or her needs if something happened to the parent.

- Parent has temporary income setback – The grandparents want to prevent a child’s temporary income setback from interfering with their grandchild’s ability to attend college or affecting their child’s retirement.

Your Recommendation

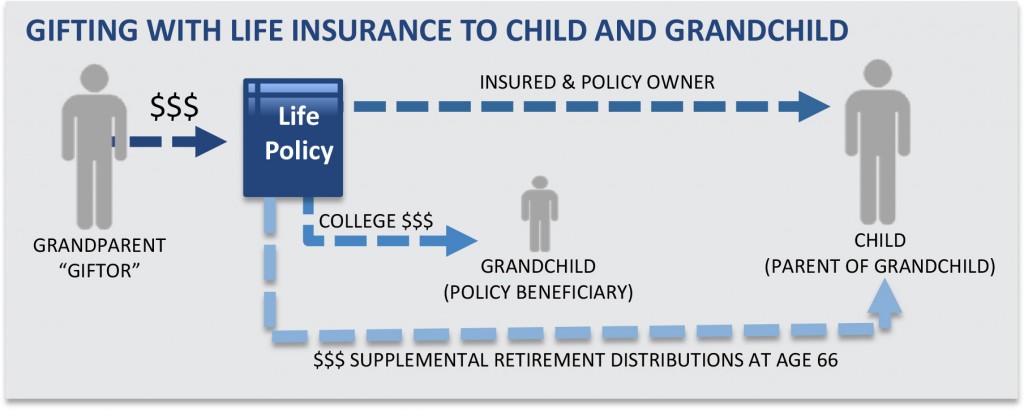

Suggest the grandparents gift the money needed to buy an IUL insurance policy on the life of their child (parent of the grandchild). The grown child will own the policy and name the grandchild (the parent’s child) as the beneficiary. The parent can access the policy’s cash value to help pay for the grandchild’s college expenses. The policy’s flexibility allows the client’s child to also access the cash value for retirement and even contribute premium payments if/when his or her financial situation improves.

Course of Action

- The grandparents gift their child $14,000 annually, the current maximum amount allowed for a single filer to prevent gift taxes, for 15 years.

- With the upside potential and no direct downside market risk of IUL, the policy has the potential to accumulate enough cash value to supplement or possibly fund the grandchild’s college.

- Depending on the client’s concerns and reasons for the policy purchase, distributions can be taken during college or provided as a “graduation bonus.” The balance of the policy will remain in-force and continue to accumulate for the child.

- Once the grown child is around age 55, he or she could contribute to the policy to build up additional cash value. The grown child pays $6,000 in annual premium for 10 years, building up the cash value for retirement income. Between ages 56 and 65 he or she can begin taking distributions from the policy.

Call your Life Sales Team today to discuss this idea and to run an illustration. 800.992.2642

FOR AGENT USE ONLY. NOT FOR USE WITH THE GENERAL PUBLIC. 13085 2013/11/21

Withdrawals will reduce the guaranteed death benefit. Surrender charges may apply to withdrawals. Taxation normally required, based on any gain at the time of surrender or transfer.

Related terms: Life, Sales Strategies

Recommended Articles

Assist Baby Boomers on the Cusp of Exiting Their Businesses You can be a valuable asset to your baby boomer clients and gain two sales in the process.

We’ve seen the reported spike in capturing the business-owner market in journals and media. […]

Assist Baby Boomers on the Cusp of Exiting Their Businesses You can be a valuable asset to your baby boomer clients and gain two sales in the process.

We’ve seen the reported spike in capturing the business-owner market in journals and media. […] A Multi-faceted Solution For A Secure Future The features and benefits of today’s indexed universal life (IUL)

A Multi-faceted Solution For A Secure Future The features and benefits of today’s indexed universal life (IUL) Above and Beyond Tax-Advantaged Retirement Options You’re meeting with an affluent client or prospect that is 10 years or less away from retirement. He’s in good shape financially, but he’s also in great shape physically, and wants to […]

Above and Beyond Tax-Advantaged Retirement Options You’re meeting with an affluent client or prospect that is 10 years or less away from retirement. He’s in good shape financially, but he’s also in great shape physically, and wants to […] IUL Sales Tool – Tax-Smart Retirement I was in your shoes. I’m a former NWM advisor who sold life insurance. Here’s a strategy I created and have shared with many advisors. This strategy has helped dozens of practices take […]

IUL Sales Tool – Tax-Smart Retirement I was in your shoes. I’m a former NWM advisor who sold life insurance. Here’s a strategy I created and have shared with many advisors. This strategy has helped dozens of practices take […]